"The initial experimental cherries underwent a manual de-hulling procedure, all by hand. 100g of green coffee absorbs 8 hours of manual labor. This led us to better understand in which direction the coffee was heading."

The amount of time and effort it has taken to just arrive at the stage to physically look at 100g of green coffee is immense. New developments, new concepts, breaking barriers does not come cheap.

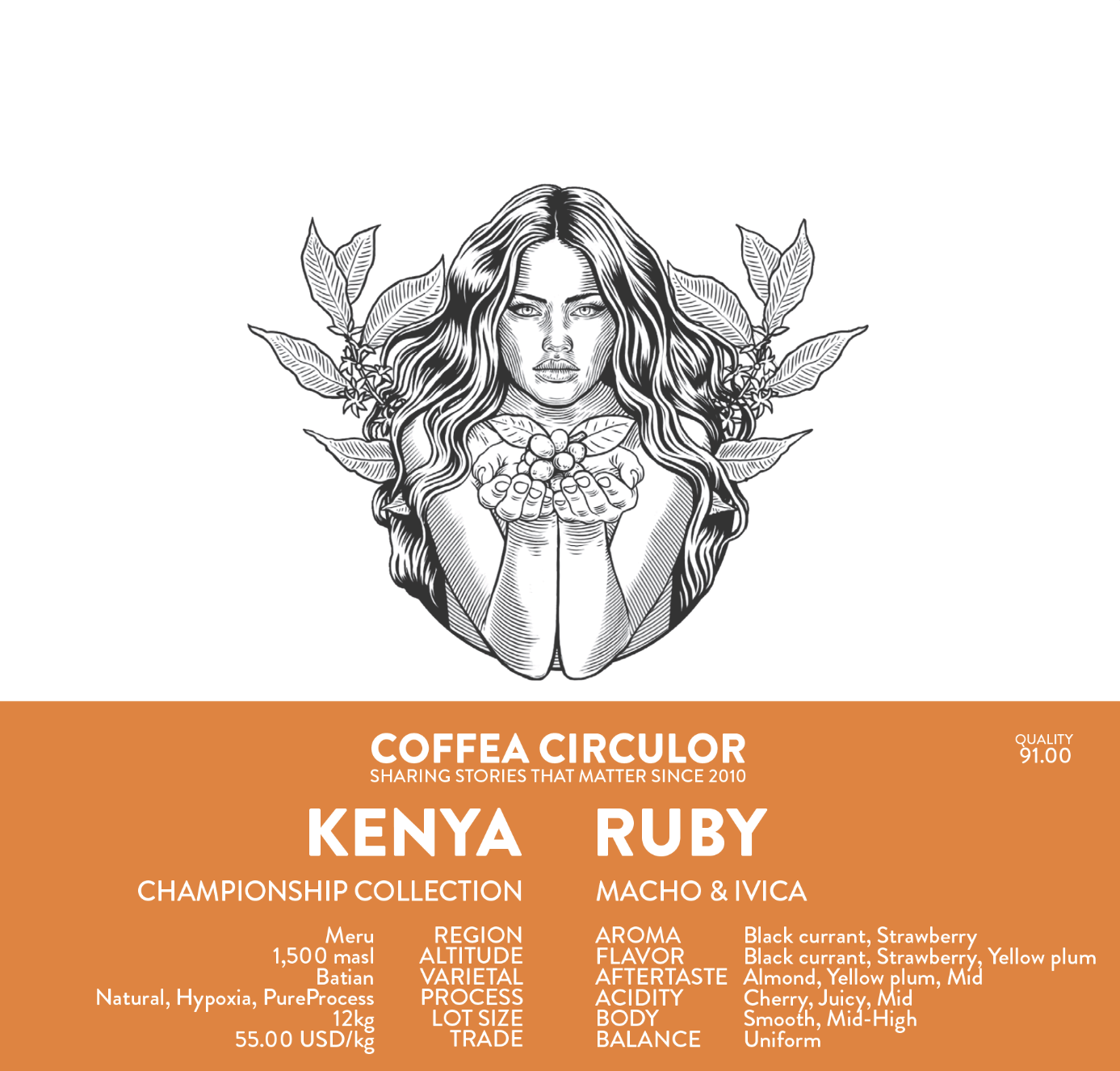

We went back to our origin, inception and birth, Meru. Our ambition was to initiate a growing program focusing on natural processing pioneering the Batian variety.

Today, Kenyan coffee producers are bringing their cherries to a washing station. Each “lot” or the ripe cherries the producer is bringing is not separated by the specific "lot". All cherries are collectively processed from other lots of producers as well. As far as we know, few or no washing stations are keeping track of which farmers are contributing with SLs, Ruiru 11, K7, Batian or alike. Therefore, when you see “third wave Kenyan coffee bags” expressing “SL28 and Ruiru 11”, it is very difficult to identify the specific percentage of each contributing variety and its final affect on sensory evaluation.

We went back to our origin, inception and birth, Meru. Our ambition was to initiate a growing program focusing on natural and experimental processing. The effect will be to lower production costs and minimize water usage for coffee production in a country that traditionally does not employ natural drying techniques. Macho and Ivica set out to generate a simple yet pure and efficient protocol to implement and preserve the flavor in the coffee cherries which transport into the green beans. The processing employs a cherry hypoxia-state to accelerate the initial fermentation over a short period of time, something we call extended aroma transport.

Contribution, mitigation and adaptation

Natural processing in Kenya will become more crucial and is a multifaceted response which addresses several problems. The price of washing coffee has also increased in Kenya. This, according to us, can be the effect of real estate brokers buying up land. Farmers are discouraged to grow and produce coffee due to small yield, washing stations are running at lower capacity which renders higher prices for washing estimated quantities of previous years. This is a snowballing effect that could have a significant impact on the future of Kenyan coffees. On another note, it already has a significant impact on the future of Kenyan coffees. It was predicted by us in 2010 that Batian will take a larger share in single origin coffees in Kenya and making up “blends”.

Today, as an example, Kenyan coffee producers are bringing their cherries to a washing station. Each “lot” or the harvest the producer is bringing is not separated by the specific "lot". All cherries are collectively processed from other lots of producers as well. As far as we know, few or no washing stations are keeping track of which farmers are contributing with SLs, Ruiru 11, K7, Batian or alike. Therefore, when you see “third wave coffee bags” expressing “SL28 and Ruiru 11”, it is very difficult to set a specific percentage of each contributing variety and its final affect on sensory evaluation. Kenyan coffees are heading towards "Ethiopian heirloom" - and that does necessarily mean it is a bad thing. This was our observation since at least 2009 and it has raised some concerns lately with our long term observations. This, according to us, is one way of preserving the Kenyan coffee heritage at its purest level.

A new take on Transparency Trade: Customer Expectancy Price (CEP) and True Development Cost (TDC)

When we set out to develop our framework for Transparency Trade in the early 2000, little did we know that the aspect of the concept was insufficient. Additionally, today in 2021, the notion of "Transparency" in coffee is a washed out concept, mainly because it is confused with the notion of "origin". It is used to express the standard issue details about coffee such as country, region, varietal, and processing. Additionally, it is widely used as a marketing ideal that is impossible to achieve based on "numbers" that are beyond ones supervision. Briefly expressed, to claim "transparency" when not having complete overview of financial traversal in coffee production is nowhere close to transparent. The only way to achieve transparency is to grow, harvest, process, mill and export coffee with proprietary methods. Only then can one understand "transparency". Claiming otherwise is smoke and mirrors. It took us almost 20 years to understand this. Nobody should be able to fool a customer to think otherwise with a marketing stunt.

"The only way to achieve transparency is to grow, harvest, process, mill and export coffee with proprietary methods. Only then can one understand and claim "transparency". It took us almost 20 years to understand this. Nobody is allowed to fool a customer to think otherwise. Claiming otherwise is smoke and mirrors - an obvious marketing stunt using terminology that is not rooted in reality and is pure ignorance."

This proprietary developed coffee also explores a socio-financial aspect of the 'specialty coffee world', namely the "Customer Expectancy Price" versus the "True Development Costs" for realizing this lot. Accomplishing this project, such as similar projects in the past, carries internal costs that are subsidized and powered by previous earnings and funding. In reality for you as a customer, when "buying one coffee bag from Coffea Circulor", you are not just buying coffee - you are also investing in future projects and products - an investment.

However, throughout the past decade we have accumulated knowledge from customer relationships where "people expect to have coffee at a decent set price whilst continuously chasing for new experiences and Wow-effects". Many examples can be rendered. Yet, few - if anybody - has asked or invested time into understanding the amount of time, energy, effort, development, administration, "real on the ground work", planning, pre-purchasing allocated cherries, idea-generating, processing, hulling, shipping, roasting, analyzing, roasting again, preparing for release. The TTR - Time To Release for these projects are much longer than any other coffees from established washing, drying and sorting stations.

The "Customer Expectancy Price" and the "True Development Cost" has to be understood. You as a customer have the equal responsibility just as much as we as producers have the responsibility to bring you an excellent coffee experience. Later, when "judging the cup", "writing a review", "criticizing this or that is lacking", think twice about the journey that each coffee producer in the world has to go through to bring the coffee to you. After all, you as a customer, is "only brewing the coffee" - a fraction of the step the coffee has to pass in the coffee value chain. Therefore, this project is anchored in a "Think Twice"-moniker. Go beyond your 3 flavor notes and understand your green coffee producer and your coffee roaster.

The accumulated cost, in short, for this coffee is 55 USD/kg as displayed. That is only for the cherries and preparation of the processing. Each 250g bag of green coffee would then be 55 / 4 = 13.75 EUR including shipping. Before even reaching that point, the level of administration, communication, (no travel in Covid-19 times), planning, payment to pickers, ... etc. is a factor that can make that 250g bag of roasted surpass 100 EUR. However, we have been very casual in our calculation and achieved a cost of 81.25 EUR per finalized 250g produced bag. In addition, we are not applying any "fancy" packaging - in order to save on costs to ensure you as a customer doesn't have to "pay more than necessary" for the most important thing: the coffee, not a package.

Perhaps this coffee can win an international coffee competition or maybe not. Perhaps it will "just be a coffee to be enjoyed". It is primarily meant to showcase what can be achieved by having a will to change and innovate. With dedicated planning, processing, collaboration and endurance. Additionally, to bring back the incentive for coffee producers in Kenya to not give up their land because "customers in the rich world doesn't want to pay for real development costs and price of coffee in general".

"You, as a customer, now have the chance to take part of this information and let it become a moment of reflection: Extraordinary coffee does not come cheap, does not come for free - there are people working on this."

Without pointing any fingers, as everyone will understand, very few if any would "want to pay" the "True Development Cost" and that is "expected".